June Overview

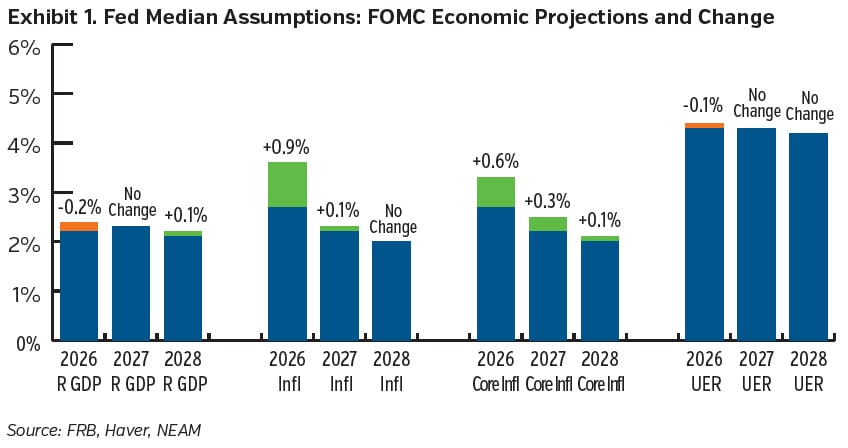

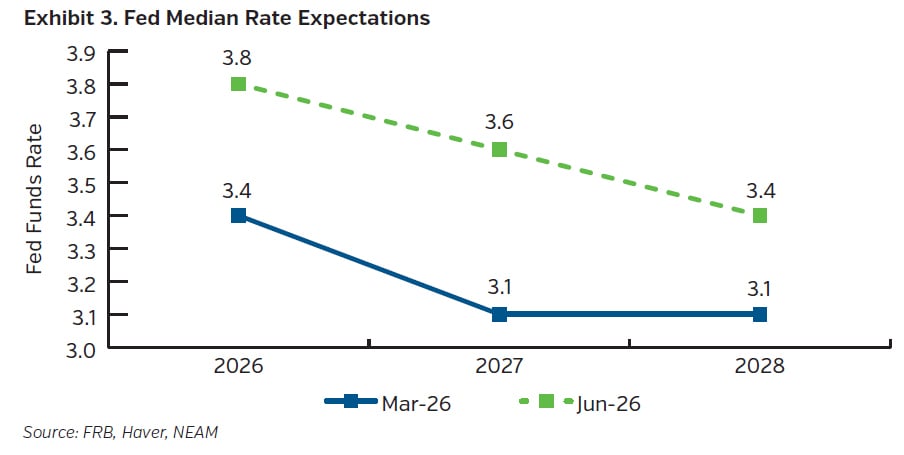

June marked the first FOMC meeting under Fed Chairman Kevin Warsh, with the committee maintaining the funds-rate target at 3.50%–3.75% in a unanimous vote. The shorter statement removed explicit forward guidance while still describing an expanding economy facing uncertainty and inflation that remains above target. The updated Summary of Economic Projections leaned more cautious: 2026 growth was trimmed, near-term inflation assumptions rose, unemployment was little changed, and the median policy-rate path shifted higher. The message is that the Fed still views activity as durable, but it is less willing to assume disinflation will resume quickly; the hurdle for easing has risen.

The June employment report reinforced the “resilient but cooling” view. Payrolls increased by just 57K after downwardly revised gains of 129K in May and 148K in April, lowering the three-month average to 111K. Professional and business services, social assistance and health care accounted for most of the gains, while leisure and hospitality, information and some cyclically sensitive sectors softened. Household employment fell and labor-force participation dropped, allowing the unemployment rate to edge down to 4.2%. The labor market therefore still supports spending, but momentum has cooled further from earlier-cycle strength.

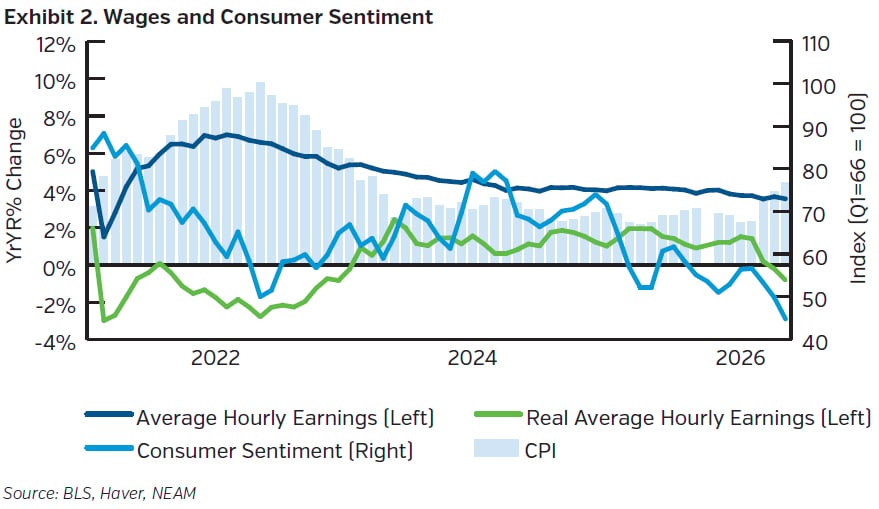

Wage growth continues to normalize. Average hourly earnings rose 0.3% in June and 3.5% over the year to $37.64, still above the pre-pandemic pace but not accelerating; real pay remains pressured as inflation runs faster than wages. The weaker payroll gain, lower participation, and “low-hire, low-fire” characterization point to a labor market that is cooling without a layoff cycle. Consumer sentiment improved 10.5% from May as gas prices moderated but remains nearly 20% below last year as high prices continue to weigh on household finances.

The Fed’s Beige Book and regional manufacturing surveys point to selective growth rather than broad acceleration. Data-center and AI infrastructure demand is supporting parts of manufacturing and business equipment, while firms remain cautious on capital expenditures because input costs, labor costs and supply-chain uncertainty are still elevated.

Industrial production was flat in May as weakness in consumer goods offset gains elsewhere. The interpretation is that corporate demand is not collapsing, but margin pressure and limited pricing power are keeping firms selective.

The BEA’s May personal income and outlays report reinforced the “sticky inflation, resilient consumer” theme. Headline PCE inflation rose 0.4% from April and 4.1% from a year earlier; core PCE, excluding food and energy, rose 0.3% on the month and 3.4% year over year. Energy was an important contributor to the headline gain, but core services and other underlying categories remained firm enough to keep inflation materially above the Fed’s 2% objective. Because PCE is the Fed’s preferred inflation gauge, the report reduces confidence that inflation is moving sustainably lower and supports the committee’s cautious tone.

The income and spending details showed why the economy can remain resilient even with tighter policy. Personal income increased $181.6 billion, or 0.7%, in May; disposable personal income rose $164.9 billion, also 0.7%. Current-dollar consumer spending increased $156.1 billion, or 0.7%, split between a $94.3 billion increase in services and a $61.8 billion increase in goods. After adjusting for inflation, real PCE rose a more modest 0.3%, while real disposable income also rose 0.3%. The saving rate was 3.0%, with personal saving at $704.2 billion. In short, households are still spending, but part of the nominal increase reflects higher prices, and the savings cushion is not especially large.

Capital Market Implications

The Fed held rates steady while emphasizing its commitment to restoring price stability. Stronger spending and firmer PCE inflation argue against near-term easing, while a cooling but still orderly labor market gives policymakers time to wait. Treasury yields and risk assets are therefore likely to remain highly sensitive to each inflation release and to evidence that real consumer demand is finally slowing.

Capital Markets

Fixed Income Returns

As geopolitical tensions eased, the Fed maintained its benchmark rate level while refining its communication style under new leadership. Inflation remains above target, and will be a continued focus of the Fed, as growth and the labor market continue to hold up. Treasury yields rose, while credit spreads stayed rangebound.

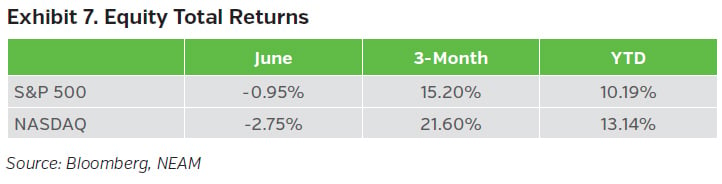

Equity Total Returns

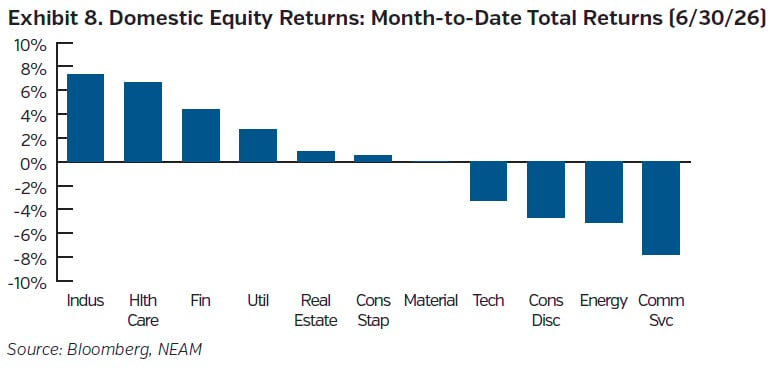

Equity indices lost ground during the month of June, primarily due to a sell-off in the technology and semiconductor sectors. This downturn was also driven by rising interest rate concerns following hawkish Fed messaging, strong jobs data, geopolitical volatility, and investor caution surrounding high AI-related valuations.