In today’s market environment, alternatives and private credit dominate the conversation. These products are marketed as innovative, differentiated, and attractive, while core fixed income is often dismissed as boring, commoditized, or merely a portfolio requirement. For some market participants, core bonds have become an afterthought, something to hold because investment policy requires it. That framing is misguided. Core fixed income does not have to be plain vanilla. When managed actively, thoughtfully, and with discipline, core fixed income can be a durable source of compounded alpha and true value creation over time.

Pitfalls of Benchmark Hugging

Many core strategies are constrained by an excessive focus on benchmarks and tracking error, resulting in portfolios that hug the index so closely that outperformance becomes mathematically unachievable. When the primary objective is to closely match the benchmark, the result is predictability but without added value. Alpha is not created by fear of deviation. It is created by judgment, selectivity, and the willingness to act when warranted by the opportunity set.

Size and scale can also hinder outperformance. Asset managers with disproportionately high AUM (assets under management) may be forced into behavior that undermines alpha generation. Large, constant inflows require participation in virtually every new issue, often regardless of relative value, simply to stay invested. The result is cash-drag avoidance at the expense of selectivity, and portfolios that increasingly resemble the index by default. Consequently, individual portfolios end up with a sizable number of small-lot positions, which can limit secondary-market liquidity.

Harnessing Yield-Driven Total Return

A core fixed income portfolio that is permitted to deviate from benchmark composition can pursue opportunities where compensation is mispriced and competition is thinner. This includes the ability to overweight spread sectors when valuations are attractive, such as non-traditional asset backed securities (ABS) offering structural protections and yield premiums, taxable municipals where credit quality and yield advantage are compelling, and preferred securities where capital structure and convexity profile enhance income without undue risk. These are not exotic bets but rather disciplined expressions of relative value that benchmark constrained portfolios simply do not access.

Importantly, sustainable alpha in core fixed income should not be dominated by duration calls. Directional interest rate bets can generate short term price appreciation, but when those calls are wrong, the recovery path is long and uncertain, particularly in low yield environments. Similarly, reaching for spread duration through lower quality credit introduces asymmetric risk. Losses on defaults are permanent impairments, and recovering from them is far more difficult than weathering mark-to-market volatility. These riskier approaches often lead to deteriorating book yields, higher turnover, elevated frictional trading costs, and a shortened investment horizon that is misaligned with the long term objectives of insurers’ core fixed income mandates.

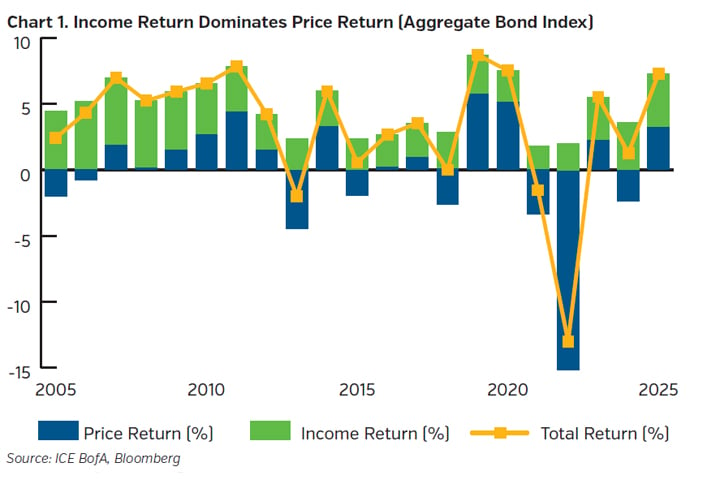

A more robust approach de-emphasizes duration as the primary driver of excess return and instead focuses on income generation and security selection, where outcomes are more controllable and repeatable. A yield-driven total return strategy sits at the center of this philosophy. Income provides a natural cushion against volatility, typically improving risk-adjusted returns over time. It supports liability management, enhances liquidity, and contributes directly to surplus accumulation, objectives that matter deeply to long-term institutional investors. Moreover, income-based returns tend to be more stable than a strategy relying on capital gains and their associated (and volatile) tax consequences.

Relative value discipline is the guardrail that makes a yield-driven total return strategy repeatable and consistent. Without a valuation framework, the pursuit of higher carry can quickly become “yield at any price,” where investors accept too little compensation for liquidity, convexity, optionality, and both credit and spread duration. A disciplined process weighs spread compensation against the risks embedded in structure and sector exposure, establishes buy and sell targets, and enforces rotation when valuations become rich, credit views change, or better forward returns exist elsewhere. The objective is simple: earn income while continuously improving the portfolio’s price-to-risk profile by harvesting sector and security mispricings, protecting yield quality, and positioning the portfolio to compound through different rate and credit regimes.

At its best, core fixed income is not a passive allocation or a risk free anchor. It is an actively managed engine of stability and incremental return rewarding patience, discipline, and selectivity. In an environment captivated by complexity and novelty, there is enduring value in executing on the fundamentals exceptionally well. Core fixed income may never be flashy, but when managed with intent, it remains one of the most reliable tools investors have for creating income consistency and lasting value.

Key Takeaways

• Core fixed income is not inherently “boring” or commoditized. When managed actively with discipline, it can be a durable source of compounded alpha and long-term value creation.

• An excessive focus on tracking error and index replication (“benchmark hugging”) makes outperformance mathematically difficult, while more flexible managers can exploit secondary-market and off-benchmark relative value.

• Sustainable excess return should emphasize risk-adjusted yield. An income-focused approach grounded in attractive relative value provides a cushion against volatility, improves consistency, and compounds more reliably across market cycles.