Private credit’s rapid expansion has prompted echoes of the subprime lending boom, raising the question of whether another financial stress event could follow. While the comparison is useful given the similarities in borrower weakness, leverage, and limited transparency, it should not be overstated. Private credit appears vulnerable to credit losses and repricing, but lacks the degree of interconnectedness, short-term funding dependence, and transmission into the banking system that made subprime mortgages systemically destructive. In the end, private credit is a market that may prove painful for some investors and borrowers, but it is less likely to trigger a broad financial shock.

Borrower Quality Is the Foundation

A noteworthy commonality between private credit and subprime is borrower quality: both markets expanded by extending capital to fundamentally weaker credits under loose underwriting standards. For the former, the borrower is a small- to mid-sized private company with financial metrics aligning with the single-B rating category, while subprime centered on borrowers with low credit scores (<620 FICO), high debt-to-income ratios, and low or no supporting income or asset documentation. A weaker starting profile leaves a borrower vulnerable to cyclical pressure, higher interest rates (in the case of floating-rate loans), limited liquidity in the event of a shock, and sector-specific disruption (as in the current threat to the software sector from AI). This matters because weak credit is the foundation of loss frequency. It does not, however, render the asset class systemic.

A Surge of Capital Fueled the Expansion

The growth pattern of private credit is also familiar. Subprime lending accelerated through securitization and an originate-to-distribute model that rewarded volume and fee generation. Likewise, private credit has benefited from private equity sponsorship, asset manager fee models, abundant “dry powder,” and investment vehicles designed to hold or distribute private loans. In both cases, growth incentives and fee structures for intermediaries and asset managers supported rapid expansion. The key difference is that private credit depends less on short-term funding conduits that amplified the subprime breakdown.

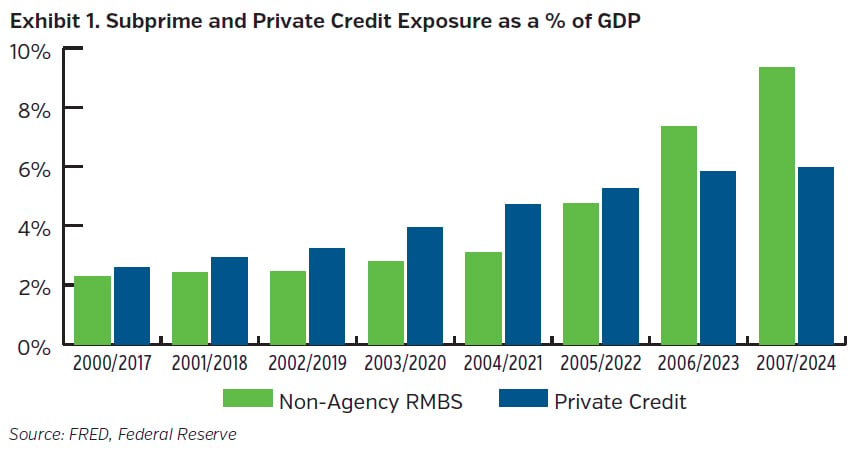

Exhibit 1 compares the path of lending expansion in both sectors as a percentage of GDP. The visual depicts a familiar theme: aggressive capital flows into both subprime and private credit during periods of easy financial conditions, compressing risk premia and accelerating weaker-credit underwriting. For investors, this parallel matters because the rapid scale-up suggests complacency around downside risk in a yield-driven lending environment.

Opacity Clouds the True Risk

Opacity is another important parallel. In subprime, layered risk was obscured by complex structures and heavy model reliance. In private credit, uncertainty stems from mark-to-model valuations, limited price discovery, reporting lags, and incomplete visibility into underlying borrower performance. These features can delay loss recognition and make asset deterioration harder to assess in real time. Even so, delayed information points to a slower and more uneven repricing process, not necessarily the kind of sudden unwind that was seen in the subprime funding market meltdown.

Funding Is Stronger Than the Assets

Leverage and liquidity are where the parallels become less concerning. In subprime, losses were amplified by highly levered securitization structures and collateral warehouse financing (~20x borrowed capital to equity). Private credit also includes leveraged borrowers (roughly 5x to 6x total debt to EBITDA) and some fund-level financing (roughly 0.5x debt to total assets), but leverage is generally lower and more concentrated at the borrower level than at the intermediary level. Liquidity is also more stable, as private credit vehicles have longer lockups and tighter redemption terms, reducing the risk of a forced liquidity dislocation even if asset quality deteriorates.

Most importantly, the transmission channel into the broader financial system appears limited. Private credit has relatively modest linkages to banks, representing a small share of non-bank financial institutional lending (<5% of total loan commitments to NBFIs1), and is more likely to transmit stress through refinancing pressure, restructurings, and delayed exits than through immediate contagion. Losses are likely to rise, borrowers in certain sectors may come under acute strain, and investors may face disappointing recoveries. But the balance of risk still points to a gradual credit adjustment rather than a systemic event on the scale of subprime mortgage lending.

Key Takeaways

• Private credit exhibits several vulnerabilities associated with subprime lending, including weaker borrower quality, leverage, and limited transparency, but important structural differences reduce systemic spillover risk.

• Opacity in valuation and reporting may mask deterioration, causing losses to emerge more slowly and unevenly than in publicly traded credit markets.

• Compared with subprime, private credit relies less on short-term funding and highly levered intermediation, which lowers the probability of a rapid liquidity shock.

• A more likely outcome is a slow-burn credit adjustment, marked by refinancing pressure, restructurings, and selective investor losses rather than rapid, broad-based contagion.

• For insurance companies with private credit exposure, deteriorating sector performance could increase refinancing risk, lead to impairment losses, and result in returns that fall short of expectations.

Endnote

1 The Federal Reserve, “Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications”, May 23, 2025.