Insurance companies continue to struggle with a low interest rate environment, forcing them to look for creative ways to stem the decline in fixed income book yields. The decline in book yield represents a decrease of 153 bps from 2007–2008. This translates to lost investment income of almost $14 billion for the P&C industry.1 The significance of the decline is twofold: first, the current low yield environment offers little additional cushion in the face of challenging underwriting conditions; second, the timeline to restore these yields is being extended, as rates remain relatively low. In this issue, we examine the potential timing and magnitude of the anticipated further book yield degradation and eventual stabilization.

CURRENT YIELD ENVIRONMENT

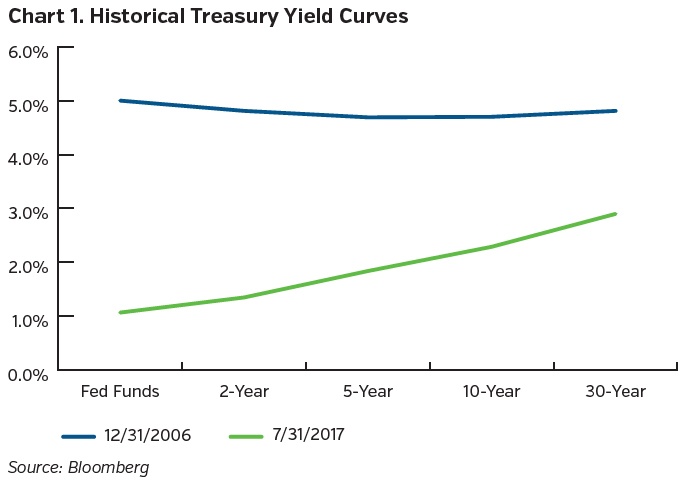

As unprecedented monetary stimulus by the global central banks eases, low growth conditions persist. Even though rates have increased since the Trump election, interest rates are nearly at historic lows across all tenors, as shown in Chart 1.

Insurance companies are among the constituencies that have suffered the most, being forced to accept lower investment income. While the timing is unclear, higher interest rates would be welcomed by P&C insurers, which expect to receive nearly $300 billion (over 30% of book value) in principal cash flows by the end of 2019.2 We explore the projected trajectory of interest rates over the next three years and the important implications it has for the P&C industry’s future investment income.

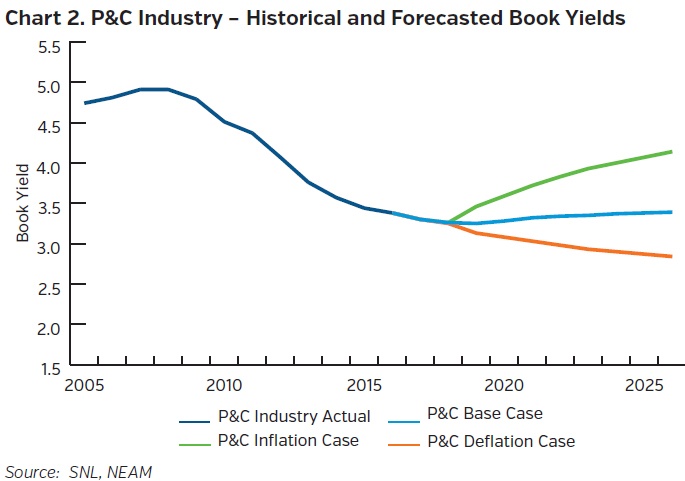

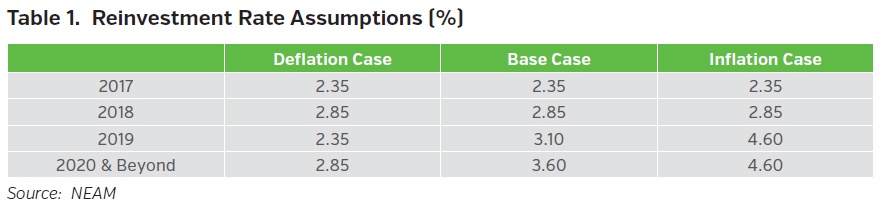

Chart 2 shows historical and projected book yields based on three potential interest rate paths: a deflation case, base case and inflation case. Table 1 shows the reinvestment rate assumptions used in the forecast scenarios.

Using our Capital and Risk Analytics (CARA®) platform’s cash flow and investment income forecast modules, we have created an income forecast for the entire P&C industry. Last year the NEAM forecast for the industry showed the book yield would be 3.36% (excluding cash) at the end of 2016. Actual year-end 2016 book yield was 3.38%, a decline of 6 bps and more than $500 million of investment income in 2016.1 This year we are forecasting the industry book yield will be 3.30% at the end of 2017, a decrease of 8 bps from year-end 2016. This would result in a decline of over $700 million of investment income for the industry in 2017. 1 In the base case scenario, the industry book yield does not return to the 3.38% year-end 2016 book yield until 2024. Even in the inflation case, where the reinvestment rate is 4.6% in 2019 and beyond, it takes until 2024 for the book yield to recover to the year-end 2012 level.

IMPLICATIONS FOR INSURANCE COMPANIES – EXAMPLE

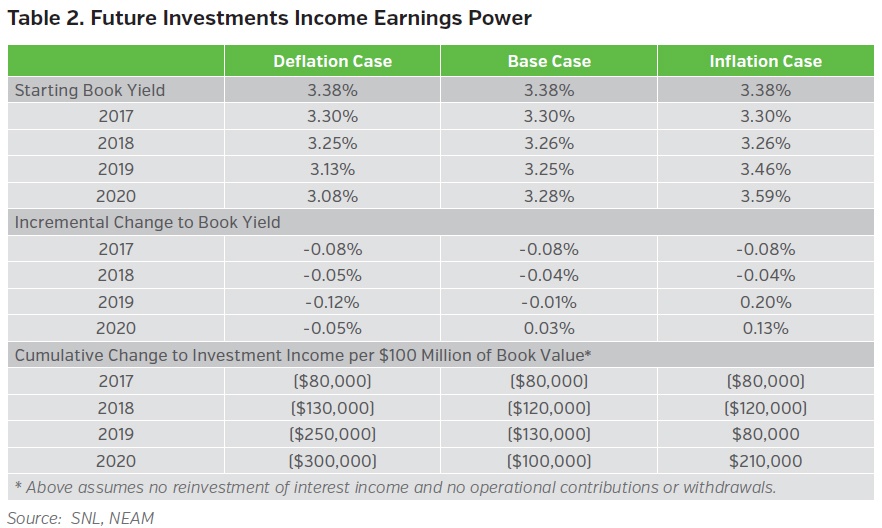

There is a measurable impact of having to reinvest at lower yields that leads to a lower margin of error for underwriting results. As older, higher yielding securities mature and the resulting cash is reinvested at market rates, investment income per dollar declines. Therefore, all else equal, insurance companies must invest more in the future to earn the same investment income. If we ignore the benefit of future contributions and reinvested income to measure the efficiency of the existing portfolio, we note that forgone future income can be material, absent changes to existing portfolios.

Table 2 shows how the future investment income earnings power of a hypothetical $100 million portfolio changes as reinvested maturities lead to different blended book yields. The impact in all 2017 scenarios is material – at ($80,000). The base case low point comes at the end of 2019 at ($130,000).

STRATEGIES TO MITIGATE BOOK YIELD DEGRADATION

In this environment, preserving and/or increasing book yields is paramount. Evaluating changes to investment strategies must be viewed within the context of overall enterprise risk tolerance as well as rating agency (BCAR) and regulatory constraints. Based on the analysis of interrelationships between insurance company business lines and current investment opportunities, there may be opportunities for insurance companies to reconfigure portfolios to improve book yield profile without increasing enterprise risk.

- Book Yields have not hit bottom and may not return to the 12/31/2016 level for years to come.

- Investment income should decline in all presented scenarios until at least 2019, absent growth in portfolio book values.

- Opportunities to reconfigure portfolios to improve investment income should be considered within the context of enterprise risk management.

- NEAM’s CARA® platform can assess and forecast insurance company investment income and book yields.

ENDNOTE

1 Figure represents annualized forgone investment income based on 12/31/16 P&C industry book value of $911 billion.

2 Represents 12/31/16 P&C Industry par value from SNL Financial forecasted through 2019 using NEAM Analytics.

NEAM’s portfolio management tools have been utilized to provide projected book yields based on certain assumptions, including reinvestment rates. Changes to these assumptions may have a material impact on results. Projected book yields do not take into consideration the effect of taxes, changing risk profiles, operating cash flows or future investment decisions and may not reflect the effect of material economic and market factors. Readers may experience different results from any projected book yields shown. Results shown are not a guarantee of future book yields.