2Q 2026 UK Economy Overview

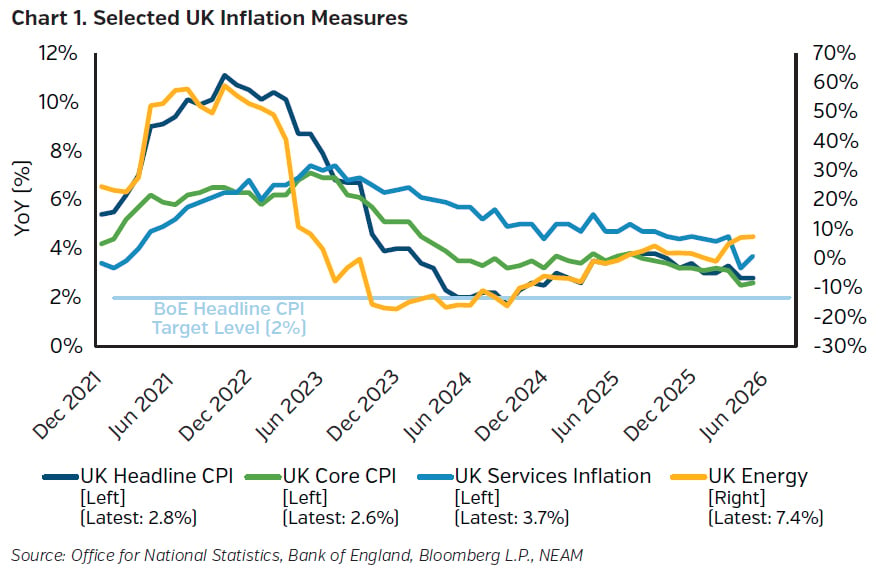

As oil prices finished the second quarter roughly US$3 above the level seen for a barrel of oil in the days leading up to the 27 February conflict escalation in the Middle East, inflation in the UK, too, fell as the quarter closed. Headline CPI rose to 3.3% in March, driven by higher fuel and energy costs, before easing to 2.8% in both April and May as lower regulated electricity prices and softer services inflation more than offset continued strength in energy inflation. In its April Monetary Policy Report (MPR), the Bank of England (BoE) had expected inflation to reach 3.0% and 3.3% in April and May, respectively. Core inflation also moderated, falling from 3.1% to 2.6% over the quarter, while services inflation declined from 4.5% to 3.7%, suggesting limited evidence of significant second-round effects thus far.

As oil prices declined following the June Memorandum of Understanding between the US and Iran, both spot prices and the futures curve moved below the assumptions underpinning Scenario A, the least inflationary scenario presented in the BoE’s April MPR. While the outlook remains dependent on the evolution of gas prices, wage growth and broader second-round effects, the fall in energy prices has reduced the risk that the more inflationary scenarios will materialise. Inflation expectations have reflected this shift in sentiment. The Citi/YouGov measure of long-term household inflation expectations fell to 3.9% in June from 4.5% in March and is now broadly in line with the average observed in the six months preceding the escalation of the Middle East conflict. Short-term inflation expectations declined more sharply, falling to 3.8% from 4.7% in May and down from a peak of 5.4% in March, returning to levels last seen at the beginning of 2026.

Economic activity weakened in Q2 following a stronger-than-expected start to the year, with Q1 GDP growing by 0.6% QoQ. The more volatile but more timely monthly GDP series contracted by 0.1% MoM in April, and most forecasters revised their Q2 growth expectations lower as the quarter progressed. Contributing to the downward revisions was the S&P Global Composite PMI, which fell into contractionary territory in May and remained below 50 through June, consistent with little or no growth in private-sector activity. At a quarterly average of 50.5, the Composite PMI was below the average reading of 52.6 recorded in Q1. The deterioration was driven primarily by weakness in the services sector, where business activity and new orders declined, while manufacturing proved more resilient, supported in part by front‑loading of activity ahead of potential disruption.

Labour market conditions softened somewhat during the second quarter, although some indicators suggested the pace of deterioration may have slowed towards quarter-end. Payroll employment rose by 2,000 in May, and April’s initial decline of -100k payrolled employees was significantly revised upwards to -53k, with estimates at the start of the tax year subject to a higher degree of uncertainty. However, payroll employment remained down 21k in total over the previous three months, continuing the negative trend seen in 2025 and Q1 2026. The unemployment rate declined modestly to 4.9% in the three months to April, although continued concerns regarding Labour Force Survey reliability limited the significance of the improvement. Wage pressures also showed signs of easing, with regular pay growth in the private sector, the measure most closely tracked by the BoE, falling to 2.9% in the three months to April from 3.1% previously.

Following Andy Burnham's victory in the Makerfield by-election and Keir Starmer's subsequent decision to resign as Labour Party leader, a leadership contest will determine the UK's next Prime Minister. Under the timetable announced by Starmer, leadership nominations are scheduled to take place between 9 July and 16 July, with any contested election concluding before Parliament returns in September. Current polling and political commentary suggest Burnham is the clear frontrunner and could assume office considerably earlier should Labour coalesce around a single candidate. In the meantime, markets are likely to focus on the prospective government's fiscal agenda, particularly its commitment to the existing fiscal rules and the extent to which it remains aligned with the 2024 Labour Party manifesto.

UK Economic Outlook

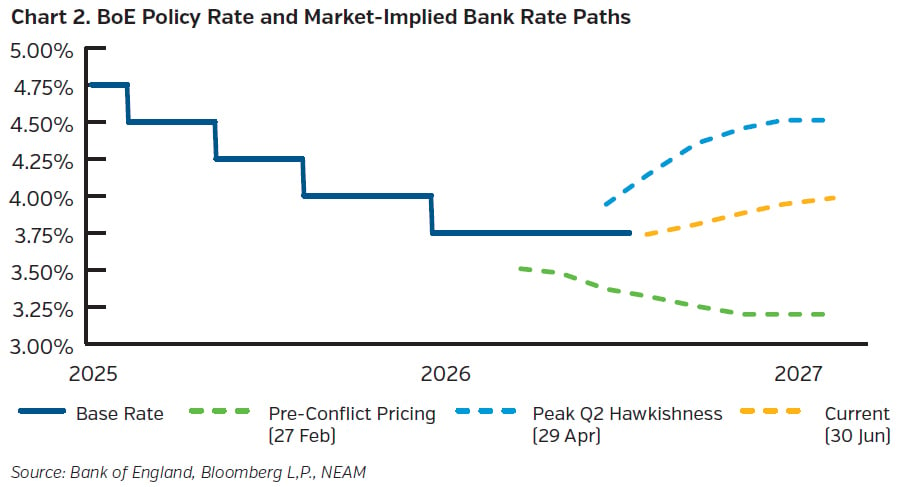

At the three meetings of the Monetary Policy Committee (MPC) of the BoE since the onset of the Iranian conflict, monetary policy was left unchanged, with the Base Rate remaining at 3.75% as policymakers sought to balance the inflationary impact of higher energy prices against evidence of a slowing economy and a loosening labour market. Faced with heightened uncertainty following the Middle East energy shock, the April Monetary Policy Report abandoned the traditional single central forecast and instead presented three alternative inflation scenarios based on differing assumptions regarding energy prices and second-round effects. Notably, the April meeting marked the first time since February 2024 that an MPC member voted to increase rates. The Chief Economist, Huw Pill, voted to raise rates, citing his belief that higher energy prices represent an inflationary shock to the UK economy and that a prompt but modest hike would help mitigate upside risks to price stability. Even as energy prices moderated in June, external MPC member Megan Greene added a second vote to increase rates, citing a desire to insure against the possibility of larger second-round effects and arguing that higher rates would help anchor inflation expectations.

As oil prices moderated during June and moved below the assumptions underpinning Scenario A, the least inflationary scenario presented in the April MPR, pressure on the Bank to tighten policy eased. Within the conditioning assumptions of the three scenarios, a common market-implied path for the Bank Rate was generated based on forward market interest rates, and at the time of publication, this rate path assumed the policy rate would peak at 4.2% in Q2 2027, implying two rate hikes over the next twelve months. Money market futures reflected this and, at one point during Q2, priced in a peak of three hikes, albeit only for a brief period. As energy prices declined in June, markets moved from pricing in two hikes at the start of June to one hike by the end of the quarter.

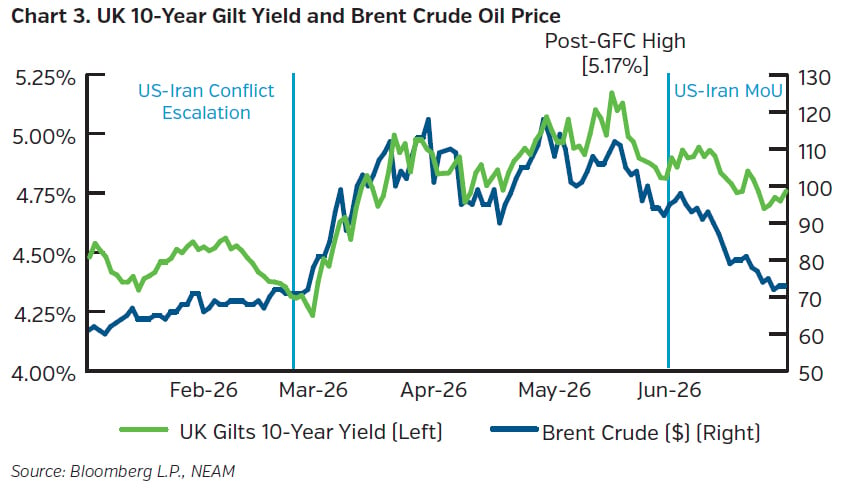

UK government bonds underwent significant bouts of volatility during Q2. The 10-year gilt yield reached a post-2008 high of 5.07% towards the end of April amid rising oil prices and growing concerns that the Middle East conflict could result in a prolonged inflation shock, before rising to a further post-2008 high of 5.17% in mid-May as the conflict appeared to re-escalate and UK political uncertainty increased. However, gilts recovered into quarter-end as hopes of a US-Iran agreement reduced inflation concerns and Andy Burnham ruled out changes to the fiscal rules, with the 10-year yield closing the quarter at 4.75%. Ultimately, the ICE BofA UK Gilt Index delivered a +2.07% total return over Q2 despite yields reaching their highest levels since the Global Financial Crisis during the quarter.