Executive Summary

The U.S. life insurance industry strengthened its liquidity amid the pandemic uncertainty. The broad sector allocations remained stable, with bonds and mortgage loans combined representing 83% of the total invested assets. Allocations to alternative (Schedule BA) assets continued to trend upward, but are predominately owned by large organizations.

Fixed income durations stayed relatively unchanged over the last five years, likely driven by asset-liability matching requirements. Over the last decade, fixed income credit quality gradually declined, while industry book yield decreased by 128 basis points (bps). The pandemic crisis and central bank actions have created a lower-for-longer interest rate environment that will continue to challenge the life insurance industry.

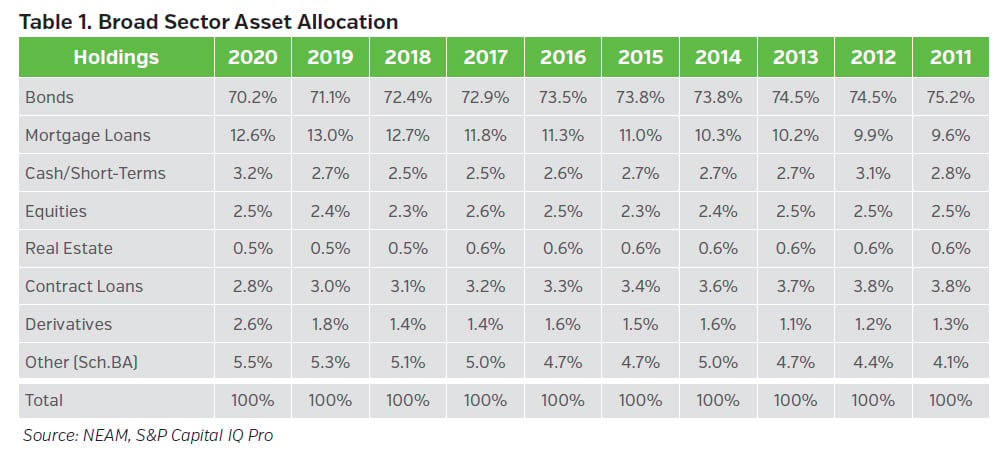

Broad Sector Allocations Largely Unchanged

The U.S. life insurance industry’s statutory asset allocation across broad sectors remained mostly unchanged during 2020 (see Table 1). Faced with the pandemic crisis and business uncertainty in 2020, the industry enhanced its liquidity through additional cash and short-term holdings. Bonds remained the largest sector, although the allocation continued to decline year over year. The allocation to mortgage loans, the second largest sector, decreased for the first time over the last decade. The allocation to Schedule BA assets reached a new high of 5.5% in 2020 and remained highly concentrated among large organizations.

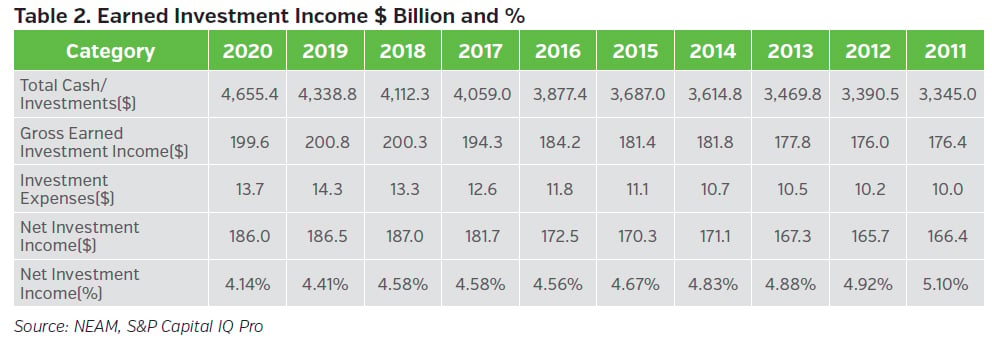

Largest Annual Investment Income (%) Decline

Table 2 highlights the industry’s earned investment income on a gross and net basis. Over the last decade, total cash and investments grew 39% from $3.3 trillion to $4.7 trillion, while net investment income ($) only increased by 12% from $166.4 billion to $186.0 billion. In 2020, the industry’s annual net investment income (%) decreased by 27 bps, which was the largest annual decline over the last 10 years.

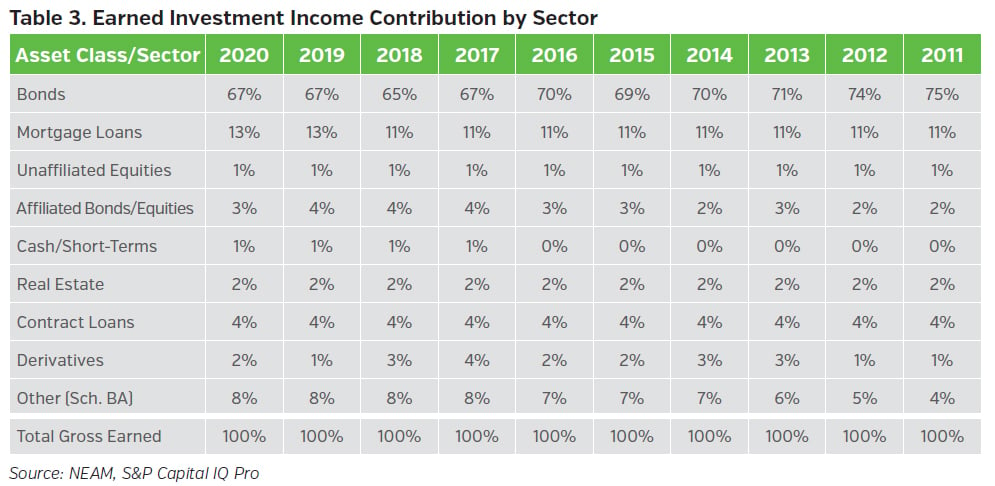

Table 3 displays the industry’s earned investment income contribution from broad asset sectors. Bonds and mortgage loans combined contributed 80% of the total, while the contribution from unaffiliated equities represented only 1%. The contribution from Schedule BA assets, which ranked behind bonds and mortgage loans, has doubled from 4% to 8% over the last decade.

Fixed Income Portfolio Details

The corporate sector represents nearly half of the aggregate fixed income portfolio (see Table 4). Private placements are the second largest sector, and the allocation has continued to increase over time. As noted in prior publications, unlike statutory Schedule D Part 1A reporting, our reported private placements category excludes any 144A securities that are publicly traded.

The allocation to structured securities (i.e., ABS, CMBS and RMBS) declined from a high of 30% prior to the financial crisis to approximately 20% in 2013 and has remained at that level. Within the structured securities, the ABS sector has continued to grow and partially offset the declining allocation from the RMBS sector.

The allocation to taxable municipal bonds rose from less than 1% prior to the financial crisis to 4.5% in 2015 and has remained at that similar level. The increase in this allocation began in 2009 and 2010, after the passage of the “American Recovery and Reinvestment Act.” This Act led to the creation of “Build America Bonds,” which allowed municipalities and municipal authorities to raise debt, with the federal government providing a direct subsidy of the interest cost.

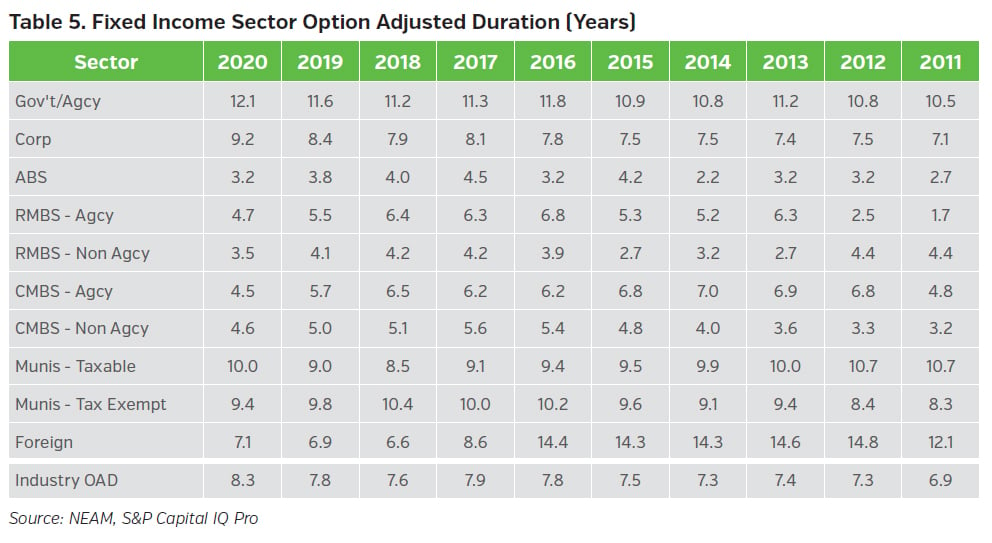

Table 5 displays option-adjusted duration (OAD) by fixed income sector. The OAD statistics are based upon CUSIP-level holdings extracted from Schedule D statutory filings and exclude any bonds held at the holding company level, derivatives, and private placement securities.

The industry’s OAD was 5.5 years right before the 2008 financial crisis and then gradually extended to 7.5 years through 2015. From 2015 to 2019, the industry’s OAD remained relatively unchanged, likely driven by asset liability matching requirements. The marginal duration lengthening of 0.5 years observed in 2020 coincided with duration extensions seen in broad corporate and government bond indices, driven by lower rates resulting from central banks’ actions to cope with the pandemic crisis.

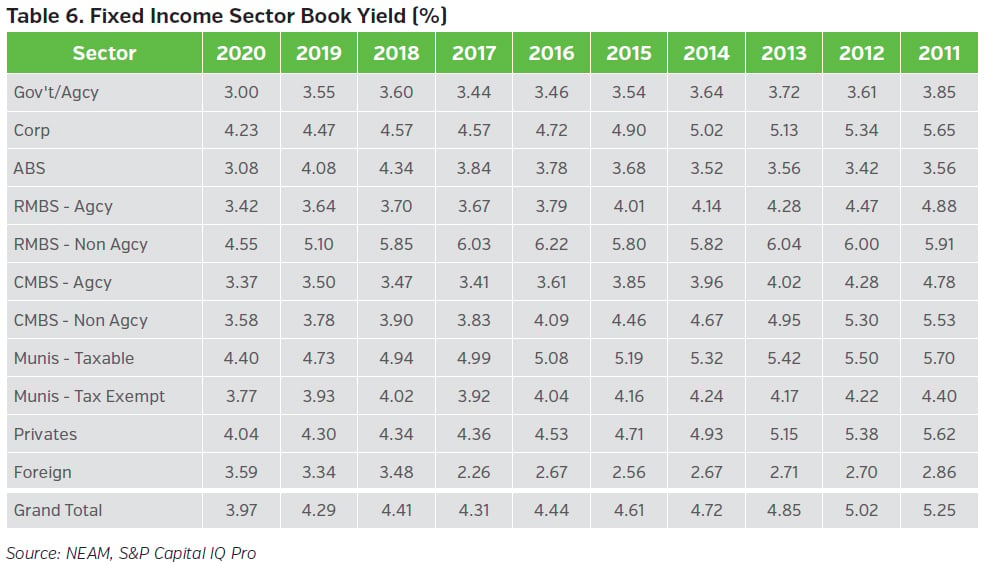

The industry’s book yield declined steadily by a total of 128 bps over the last decade (see Table 6). In 2020, the overall book yield experienced the largest annual decline of 32 bps, with ABS showing the most reduction of 100 bps. Yield declines were observed virtually across all sectors. Cumulative reductions of 191 bps in the book yields of Agency and Non-agency CMBS since 2011 reflect the runoff of seasoned pre-crisis exposures with higher embedded book yields.

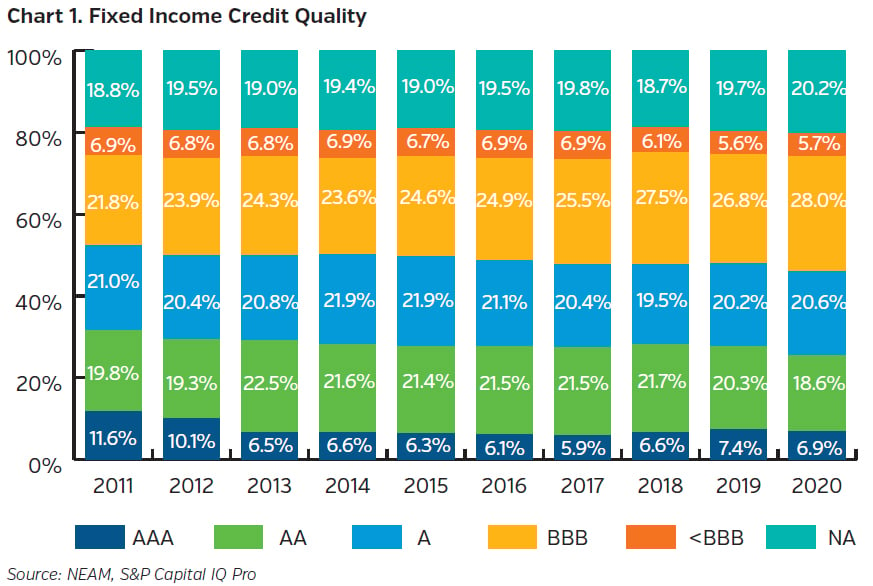

Over the last 10 years, the allocation to AAA, AA, and A securities (NAIC 1 category) decreased from 52.4% to 46.1%, while the BBB category increased from 21.8% to 28.0% (see Chart 1). The BBB allocation grew sizably over the last year, outpaced only by the increase that occurred from 2011 to 2012. The below investment grade (<BBB) allocation declined from highs of 6.9% from 2011 to 2017 to the lowest 5.7% at year-end 2020.

The NA category consists of mostly “true”1 private placement securities, which accounted for 17.8% of total fixed income holdings in 2020 (see Table 4). Based on historical statutory filings, about half of the industry’s private placement securities fell into the BBB (NAIC 2) rating category. This is much higher than the BBB allocation observed in public fixed income securities (see Chart 1).

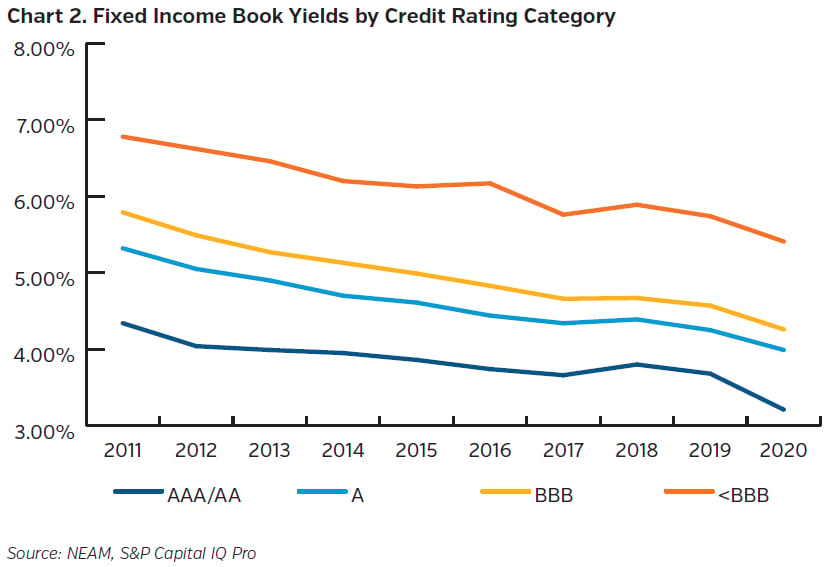

Chart 2 displays the book yields for public fixed income securities by credit rating category. In 2020, total fixed income book yields declined across all rating categories. Over the past 10 years, the higher rating categories, AAA and AA, experienced the least reduction (113 bps), while the BBB category experienced the most (153 bps).

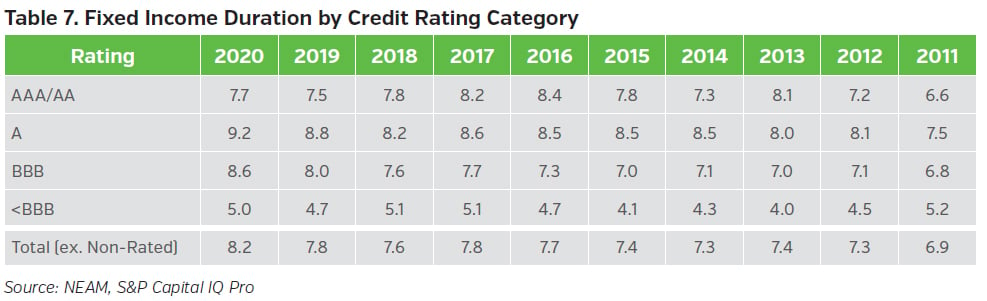

Table 7 displays the OAD for public fixed income securities by credit rating category. High yield (<BBB) bonds typically exhibit shorter durations than investment grade bonds. Over the last decade, durations extended across all rating categories, except for the <BBB category where durations remained stable. Non-rated securities (primarily private placements), which accounted for 20.2% (see Chart 1) of total fixed income holdings in 2020, were not included in the aggregate duration calculation.

Key Takeaways

- Faced with pandemic induced uncertainty, the life insurance industry strengthened its liquidity through increased cash and short-term holdings. The allocation to mortgage loans declined in 2020 for the first time in the last decade.

- The allocation to Schedule BA assets continued to rise amid the challenging low-rate environment. These alternative assets contributed to 8% of the industry’s investment income and remained highly concentrated among large organizations.

- Within the fixed income portfolio, allocations to private placement securities and ABS continued to trend upward, while allocations to RMBS, government and agency bonds exhibited declines.

- In 2020, the industry’s overall book yield experienced the largest annual decline of 32 bps over the last decade. Fixed income duration remained relatively unchanged over the last five years, presumably driven by asset liability matching requirements.

- Although the industry’s high yield (<BBB) allocation reached a new low in 2019, the BBB allocation for public fixed income securities had risen steadily since 2011. Private placements, which represented 17.8% of the total fixed income holdings in 2020, comprise approximately 50% of BBB (NAIC 2) rated securities.

- The pandemic situation and central banks’ actions have resulted in a challenging low-rate environment for the industry. Insurers should consider a holistic enterprise framework when considering taking additional risks in pursuit of investment returns.

Please contact us if you would like to receive a customized assessment, which facilitates in-depth comparisons and contrasts of enterprise characteristics of your company relative to peer organizations. The assessment supports decisions with enterprise risk preferences and investment strategy.

Endnote

1 “True” private placement category excludes any 144A securities that are publicly traded.